.avif)

A self-initiated qualitative research report by NetBramha, to understand how trust in financial products is really built, tested, and broken.

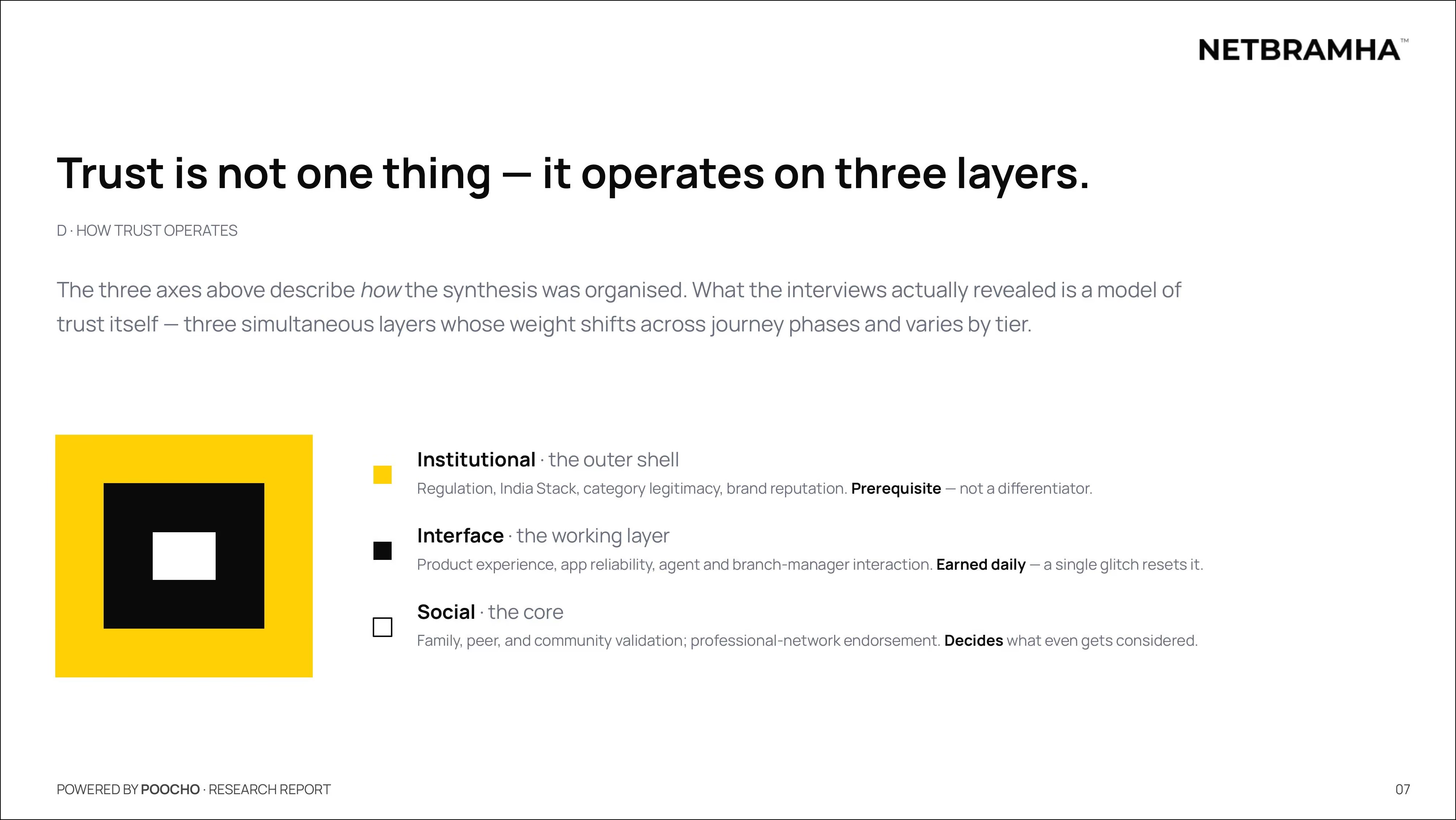

Trust in Indian financial decision-making is not a single emotion. It is a three-layer architecture, and most financial products are only designed for the outermost layer.

Social trust, which means family, CAs, and peer networks, decides what even gets considered. Before anyone opens your app, someone they trust has already voted on it.

A single technical glitch is sufficient cause for permanent switching. Not a reason to complain. A reason to leave.

First-time users cap their trial at Rs. 3,000 to Rs. 10,000 regardless of what the product promises, then observe for 4 to 12 months before committing more. This is not hesitation. It is deliberate risk management.

82% of participants explicitly refused to trust financial advice from automated tools without human validation first.

Every financial product in India is fighting for the same thing: trust. But most are fighting on the wrong battlefield.

The industry spends enormous energy on regulatory compliance, brand building, and interface polish. These matter. But they are prerequisites, not differentiators. They get you into consideration. They do not get you chosen.

We wanted to understand the deeper architecture of how Indians actually decide whom to hand their money to. Not what they say in surveys. What they actually do: the sequence of checks, the emotional states, the moments where trust breaks, and the conditions under which it can be rebuilt.

Between April 3 and April 13, NetBramha conducted qualitative research on the Poocho platform. We spoke to participants between the ages of 20 and 50, drawn from across India and grouped by tiers of digital-financial engagement. We moderated the sessions, coded the transcripts using thematic analysis, and synthesized 841 pages of source data into the framework you will find in this report.

What emerged was not a list of features users want. It was a model of how trust actually operates, and it has real implications for product design, marketing strategy, and policy.

We conducted qualitative interviews across three tiers of digital-financial engagement.

Tier 1 - Digital-first

Self-directed, app-native users who initiate financial decisions through digital interfaces. They evaluate products through app store ratings, peer validation within tech-savvy networks, and transaction performance.

Tier 2 - Peer-influenced

Users who rely on trusted intermediaries, including family members, Chartered Accountants, and relationship managers, to validate financial choices before acting. Social trust is the primary entry point.

Tier 3 - Non-digital

Users who depend on physical branches, agents, and human intermediaries for all significant transactions. The agent is not just a guide. For many, the agent is the trust itself.

Before this research, the assumption was that trust was a function of two things: brand credibility and product experience. The interviews made clear a third layer was being missed entirely, and it was the most important one.

The three-layer model above is the backbone of this report. Each layer operates differently, breaks differently, and must be designed for differently. What follows is what we found about each one.

Layer 1 - Institutional (the outer shell)

Regulation, India Stack infrastructure, category legitimacy, brand reputation. This is the prerequisite. Without it, a product does not enter consideration. But it is not what earns loyalty and it is not what keeps it. It is table stakes.

Layer 2 - Interface (the working layer)

App performance, transaction speed, reliability, confirmation clarity, agent and branch-manager interaction. This layer is earned daily. It is also the most fragile. A single glitch in a critical moment, such as a failed transaction, a delayed confirmation, or an error on a large transfer, is sufficient cause for permanent switching.

Disha, a Tier 1 participant, described her reasoning plainly: "Google Pay started having technical issues and glitches, so I shifted to PhonePe." That was it. No second chance. No complaint lodged. A permanent decision made in one moment.

Layer 3 - Social (the core)

Family recommendations, the CA who manages your accounts, the WhatsApp group where someone posted a review, the colleague who mentioned it last week. This is the layer that decides what even gets considered. Before any interface is opened, before any brand impression is formed, the social layer has already filtered the options.

For Tier 2 users, this is decisive. Nimeshgiri, whose CA manages his accounts, described his reasoning simply: "Because he himself is a CA, a Chartered Accountant, he handles all my accounts, so that's why I trusted him."

For Tier 3 users, the agent is not a channel. The agent is the trust. Abarna had never visited the LIC office her agent manages: "He isn't just a trusted person, he is the trust."

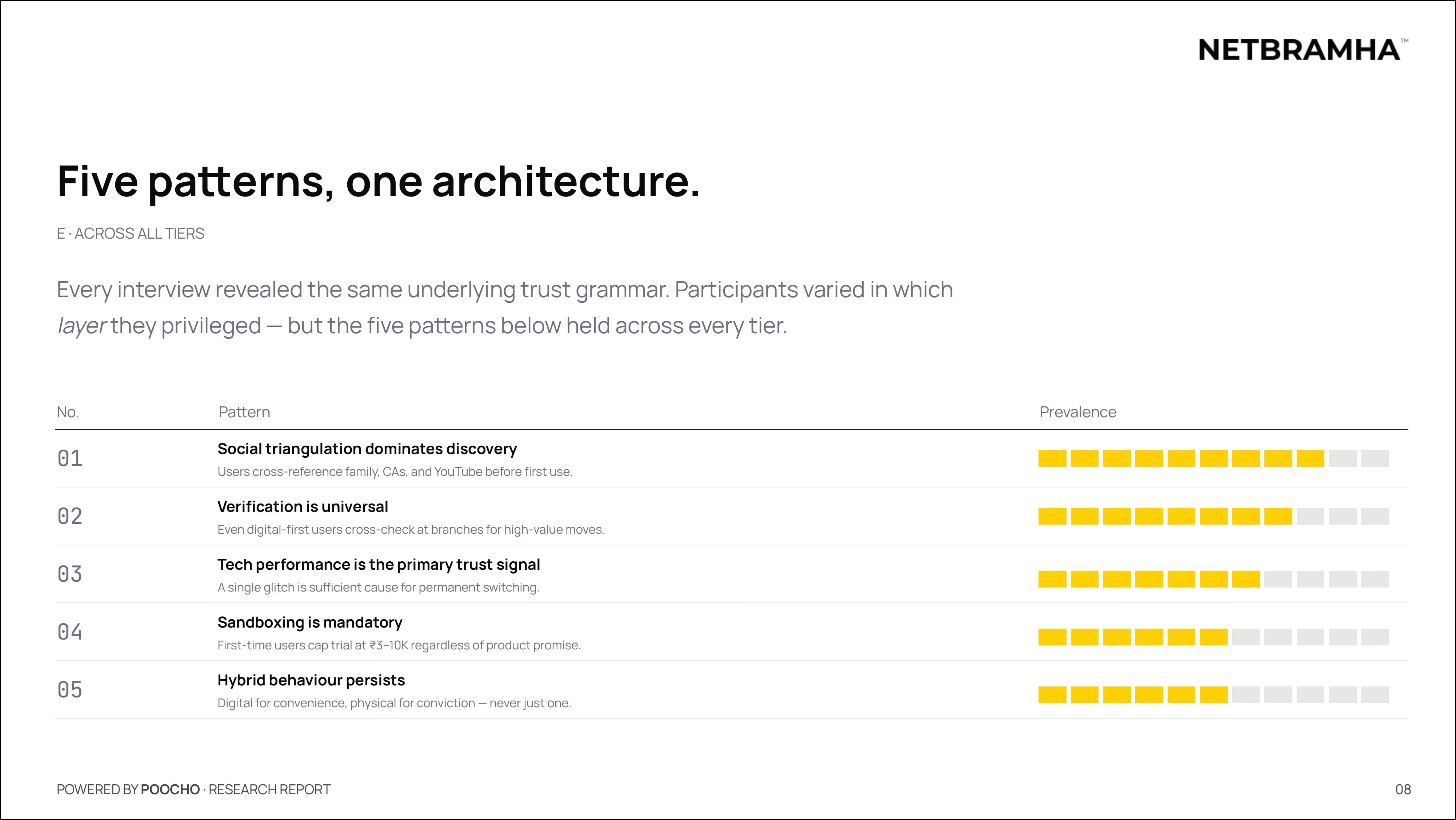

Every interview, regardless of tier, city, age, or income bracket, revealed the same underlying trust grammar. Participants differed in which layer they weighted most heavily. But these five patterns were universal.

01. Social triangulation dominates discovery

Before a first transaction, users do not open the app and explore. They cross-reference. Family members, CAs, YouTube channels, WhatsApp groups. No tier skips the social step.

02. Sandboxing is mandatory

First-time users set a trial cap regardless of what the product promises. Tier 3 starts with Rs. 3,000 to Rs. 5,000. Tier 1 and Tier 2 go up to Rs. 10,000. Then they watch. For months. Only after incident-free performance does capital commitment grow. This is not irrational caution. It is a structured, near-universal protocol.

03. Tech performance is the primary trust signal for digital users

For Tier 1, the interface is everything. What feels like a minor technical bug to a product team reads as a credibility collapse to the user.

04. Verification is universal

Even digital-first users cross-check at physical branches for large transactions. No tier trusts exclusively through digital channels when the stakes are high enough.

05. Hybrid behaviour persists, and it is deliberate

Digital is used for convenience. Physical is used for conviction. Users maintain both channels deliberately and switch between them based on transaction size and emotional stakes.

The full report unpacks each pattern by tier, with participant quotes, prevalence data, and the specific conditions under which each pattern breaks down. The page above shows you the shape. The report shows you the depth.

Trust is not a state. It is a process. Across every tier, that process followed the same sequence.

Stage 1 - Initial credibility check

Verify via regulatory status, brand reputation, app store ratings, peer recommendations.

Stage 2 - Low-stakes trial

Test with Rs. 3,000 to Rs. 10,000. Not hesitation. Deliberate risk management.

Stage 3 - Extended observation

Monitor for 4 to 12 months. Watch for glitches, unexpected behaviour, hidden charges.

Stage 4 - Gradual capital increase

Only after incident-free performance does commitment grow.

Stage 5 - Peer validation

Only then do users recommend. Never before personal, months-long experience.

The implication for product teams is significant. You are not designing for adoption. You are designing for the beginning of a trust journey that takes up to a year to complete. The goal of onboarding is not to get someone through KYC. It is to not trigger the emotional state participants described as "backstepping", a withdrawal that happens when something feels off in the first five minutes.

Across all tiers, the non-negotiables were consistent.

Regulatory oversight is mandatory. The absence of a visible regulatory signal is an immediate red flag.

Technical glitches are unacceptable. Failures are not a cost of doing business. They are a reason to leave.

Human support must be available. Even Tier 1 users expect to reach a human when needed. Availability matters more than frequency of use.

Transparency is a moral requirement. Hidden charges are not interpreted as a design oversight. They are interpreted as evidence of dishonesty. The word participants used repeatedly was "manipulation", a moral category, not a UX one.

The research also surfaced four contradictions that users hold simultaneously, without resolution. These are not bugs in user thinking. They are design challenges the industry has not yet solved.

Wanting 24/7 self-service, and wanting human support. Users see these as complementary, not competing.

Trusting regulation, and fearing hidden charges. Regulation prevents fraud. It does not prevent opacity about fees.

Avoiding complexity, and wanting sophistication. Simple for daily tasks. Deep analytics for power use. The balance is unresolved in most products.

Self-blame for fraud, and expecting protection. Users blame themselves for losses while simultaneously expecting systemic protection. The industry has not given them clear mental models of where responsibility lies.

82% of participants explicitly refused to trust financial advice from automated systems without human validation first. The response pattern across tiers was the same: start small, observe for months, consult a trusted professional before committing more.

The path to adoption of automated advice in Indian financial services runs through the CA and the relationship manager, not around them.

3 tiers, and 841 pages of source data, one thing was clear.

Trust is not granted. It is earned in stages, over months, through consistent performance, validated by people who already trust each other, and reset permanently by the first significant failure.

The products that will build durable financial relationships in India are not the ones with the most features. They are the ones that understand what trust actually means for their users, and design every layer of their experience accordingly.

The full report, 30 pages with 90 citations, the complete trust framework, tier-specific findings, journey phase analysis, and implications for product, marketing, and policy, is available to download below.

Research conducted by NetBramha from April 3 to 13, 2026. Research design, moderation, thematic analysis, synthesis, and report by NetBramha Studios. Participant recruitment and session management via Poocho.

3 tiers · 90 citations · 841 pages of source data